Range Expansion day on the back side

Trading notes for 2026-01-15

By Sean WeldonTL;DR

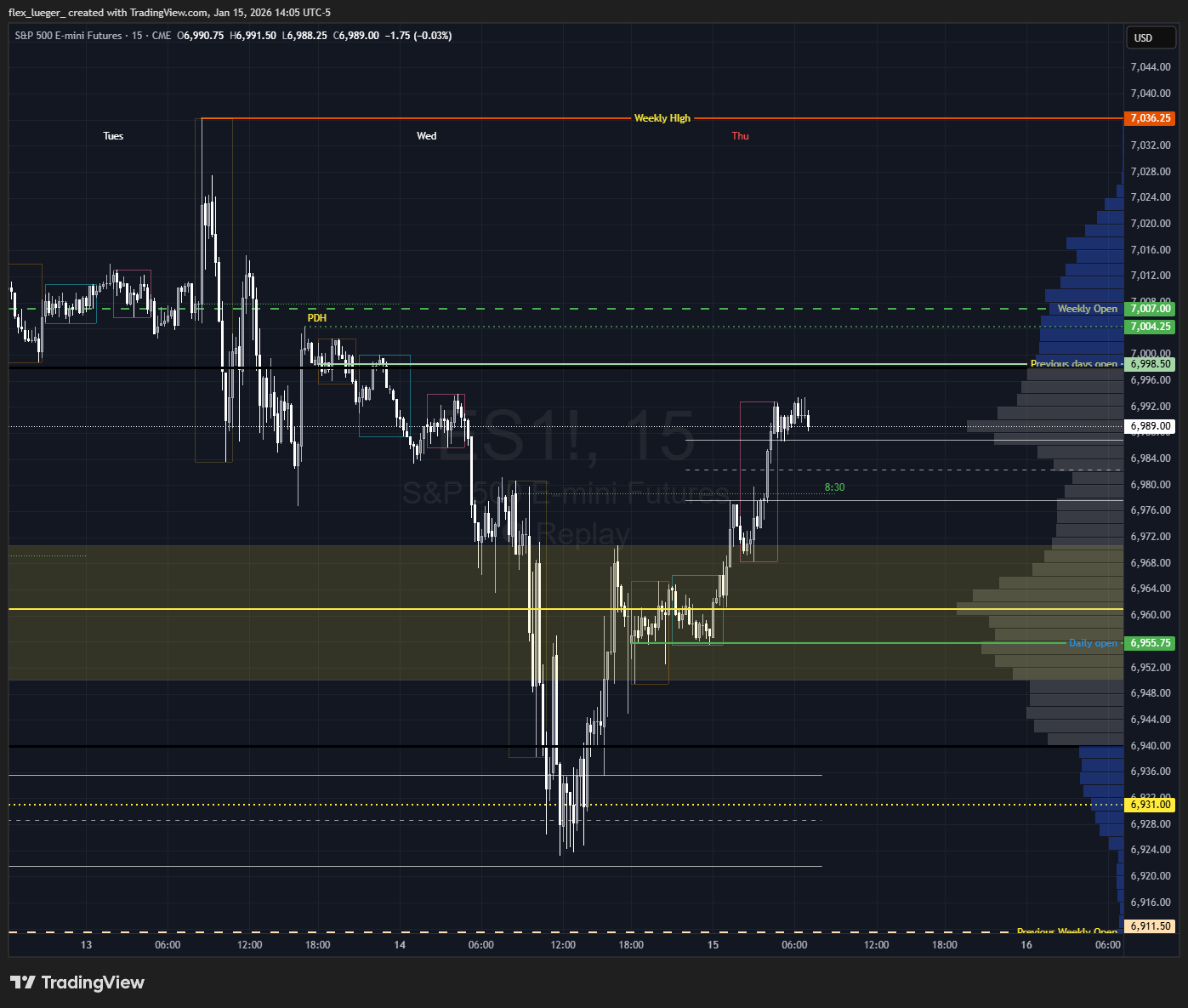

After a strong overnight rally from Wednesday's 2.5 STDV selloff, I entered a 0DTE long call at ES 7000 expecting continued bullish momentum to weekly highs. Despite price holding above my strike and maintaining 60 delta, time decay killed the position as the market stalled rather than trending explosively higher.

Market Context

The market had hit 2.5 standard deviations to the downside on Wednesday, taking out daily lows before staging a significant recovery. The overnight session through Asia and London showed strong bullish momentum, with the rally continuing into the New York session. This type of action after an extended selloff often sets up range expansion scenarios where the market can push back toward recent highs.

Thesis & Plan

My bias going into Wednesday morning was bullish, expecting a range expansion day that would push price back toward the weekly highs. The overnight strength supported this view, and I anticipated the New York open would bring additional buying pressure that could fuel a trending day higher. The setup looked prime for momentum continuation after the previous day's oversold bounce.

Entries & Exits

I entered a long call position right at the New York open, targeting the 7000 level on /ES with a 0DTE option. The plan was to capitalize on what I expected would be explosive upward movement as the market trended toward the high of the week.

What Worked / What Didn't

The directional bias wasn't entirely wrong - price did hold above my 7000 strike and maintained relatively stable levels. However, the execution was severely flawed. Instead of the explosive push I anticipated, the market consolidated and chopped around without significant directional movement.

The 0DTE structure became my worst enemy. Even with the position maintaining a 60 delta - indicating the market was behaving somewhat as expected directionally - time decay absolutely destroyed the position value. I watched helplessly as theta burn ate away at my premium throughout the session.

The market's behavior highlighted a critical flaw in my analysis: after the strong overnight rally, the market was already extended. Expecting additional explosive movement from an already stretched position was unrealistic. The smart money had likely already positioned during the overnight session, leaving little fuel for a dramatic trending day during regular hours.

Risk Management

My risk management was inadequate for this trade structure. Using 0DTE options requires extremely precise timing and explosive movement to overcome the accelerated time decay. I failed to account for the high probability that even a correct directional bias might not generate enough movement to offset theta burn.

The position sizing and time frame mismatch created unnecessary risk. Given the extended nature of the overnight move, a more conservative approach would have been warranted.

Lessons Learned

Several critical lessons emerged from this losing trade:

• 0DTE options require explosive movement - These instruments are not suitable for moderate directional plays. They demand significant, immediate price action to overcome accelerated time decay. Reserve 0DTE strategies for setups with high probability of dramatic moves.

• Consider market extension - When the market has already moved significantly (as it had overnight), expecting additional explosive movement becomes less probable. Extended markets often consolidate rather than trend further.

• Time frame selection matters - A 1DTE option would have provided more breathing room for the thesis to play out without the crushing time decay pressure. The additional day would have allowed for a more measured approach to the anticipated move.

• Volatility considerations - In hindsight, short strategies might have been more appropriate given the potential for volatility expansion and premium increases as the market worked through its post-selloff dynamics.

• Delta doesn't guarantee profitability - The shocking reality that a 60 delta position could still be severely negative reinforces how powerful time decay can be in short-dated options. High delta alone isn't sufficient to overcome structural headwinds.

This trade serves as an expensive reminder that proper instrument selection is just as important as directional accuracy. Even when reading market dynamics correctly, poor execution through inappropriate time frames can turn winning ideas into losing trades. Moving forward, I'll reserve 0DTE strategies for only the highest conviction setups with clear catalysts for immediate, explosive movement.