End of week liquidity run

Trading notes for 2026-01-16

By Sean WeldonTL;DR

Got caught adding to positions at market highs yesterday when ES consolidated at daily ATR levels before retracing past 50% equilibrium. Market seems to consistently move opposite to my thesis, suggesting I may be aligned with majority sentiment that market makers exploit. Key lesson: most moves happen the week before OPEX, while OPEX day itself shows pinning behavior around gamma levels.

Market Context

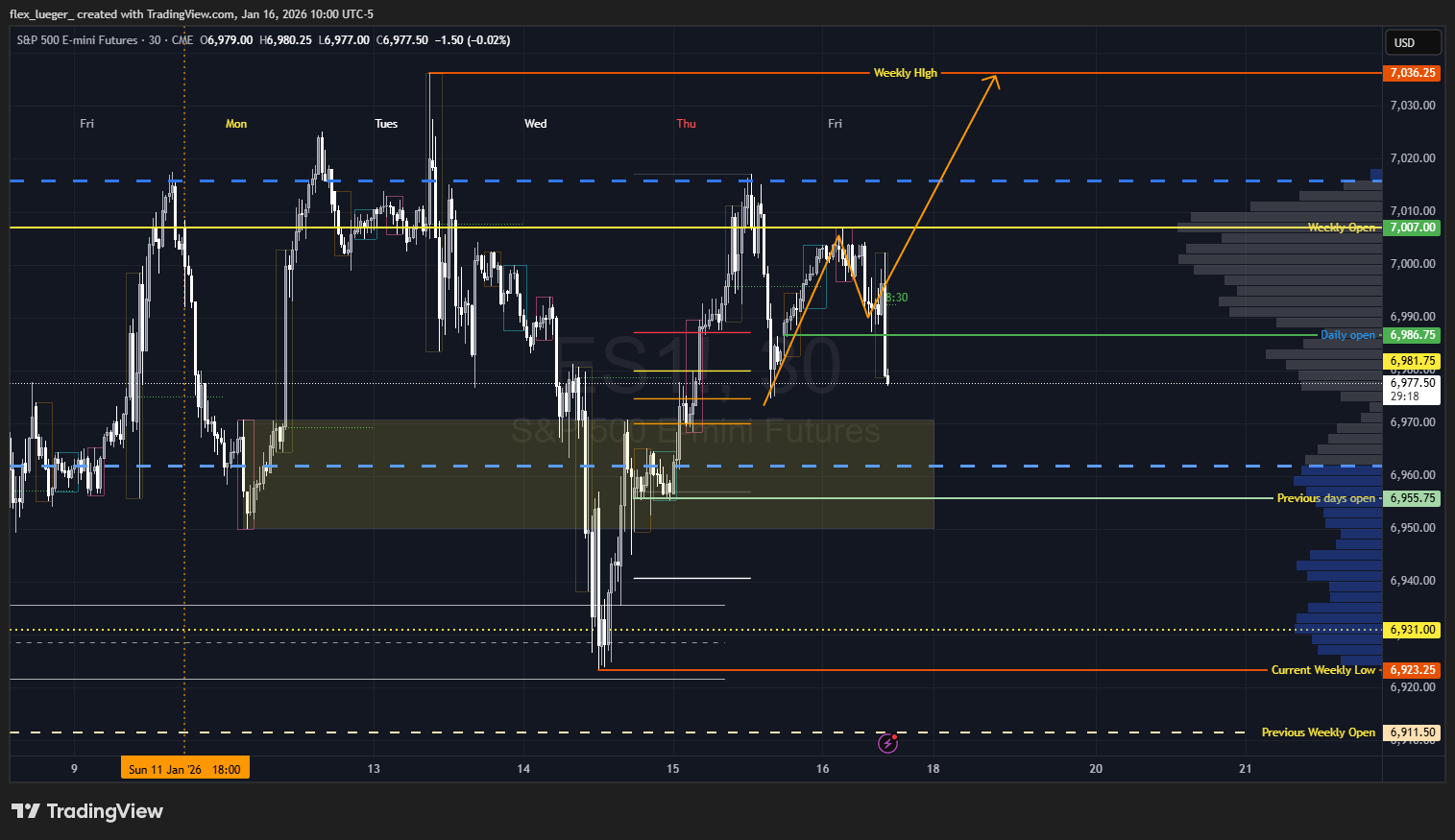

The market reached its average true range (ATR) for the day and consolidated at the highs throughout the entire New York session before dropping into a perfect retrace past the 50% equilibrium level heading into the close. This action occurred on what appears to be OPEX-related trading, with the market showing classic pinning behavior around key gamma levels.

At 12:30 PM, we saw a textbook liquidity grab as the market ran to take out the obvious low where most long positions would have their stops positioned. After triggering these stops, price reversed back into the initial balance range but struggled to push past the daily open price, showing the classic rejection at a key reference level.

Thesis & Plan

My original thesis was looking for long opportunities, with a specific entry target around the 50% equilibrium retrace level. However, I deviated from this plan and took on additional risk by adding positions at the daily highs, which proved to be poorly timed.

The more concerning pattern I'm noticing is that the market consistently moves opposite to my thesis. This is leading me to question whether my view represents the majority sentiment that market makers are actively working against to exploit common pain points.

Entries & Exits

Yesterday's trades were problematic as I added to long positions at the market highs when ES was consolidating at its ATR levels. This violated my original plan of waiting for the 50% retrace entry.

Right before market close, I entered another long position, but this time structured it as a debit spread to mitigate time decay. The position consisted of:

- Long call at 6980 on /ES

- Short call at 7000 on /ES

This spread structure helped reduce the theta burn that would have impacted a naked long call position.

Risk Management

The risk management lesson here was painful but clear. By adding at the highs instead of waiting for my planned entry, I took on unnecessary risk at an unfavorable location. The debit spread entry near the close was a better risk management decision, as it limited both downside risk and time decay exposure.

The market's move to take out obvious stops below the lows demonstrates why stop placement needs to account for these liquidity runs. Most retail longs had their stops in the obvious location, making them easy targets for institutional players.

What Worked / What Didn't

What didn't work:

- Adding to positions at daily highs instead of waiting for the planned retrace entry

- Fighting against what appears to be market maker manipulation of common retail sentiment

- Using open-ended options positions that are vulnerable to time decay and gamma pinning

What worked:

- Recognizing the need to adjust position structure with the debit spread

- Identifying the liquidity grab pattern at the lows

- Understanding the OPEX dynamics and gamma pinning behavior

Lessons Learned

The most significant lesson from this sequence is understanding OPEX week dynamics: the majority of directional moves occur in the week leading up to options expiration, while the actual OPEX day tends to exhibit pinning and mean-reverting behavior around key gamma levels.

This insight completely changes how I should approach these periods. Instead of fighting the pinning action on OPEX day, I should be positioning for the directional moves in the preceding week and then expect consolidation and mean reversion on expiration day itself.

Another critical realization is questioning whether my views align too closely with retail sentiment. If the market consistently moves opposite to my thesis, it suggests I may be part of the majority that market makers target for liquidity. This leads to two potential strategies:

- Continue developing my standard thesis but look to fade my own view

- Wait for my thesis to be exploited at maximum pain points, then enter after the liquidity grab

Moving forward, I'm eliminating open-ended calls and puts from my strategy. Instead, I'll focus on:

- Selling credit spreads to benefit from time decay and range-bound action

- Using debit spreads when directional bias is strong, to limit risk and reduce theta exposure

The liquidity grab at 12:30 PM was a perfect example of how obvious technical levels become magnets for stop runs. The market efficiently swept the lows where retail stops were clustered, then immediately reversed back into the day's range. This reinforces the importance of either positioning stops in less obvious locations or using options structures that don't require traditional stop losses.

Understanding that OPEX day behavior is fundamentally different from the rest of the week will help me avoid fighting against gamma pinning forces and instead position for the mean reversion and consolidation that typically characterizes these sessions.