10-21-25-day-2-gamma-squeeze-possibly

Trading notes for 2025-10-21

By Sean WeldonTL;DR

Identified potential day 2 continuation setup after Monday's trending session ended at highs, but market opened with a liquidity grab to new lows before recovering above opening price. Set up long debit spreads on MSTR and SPY while considering IBIT as additional gamma play.

Market Context

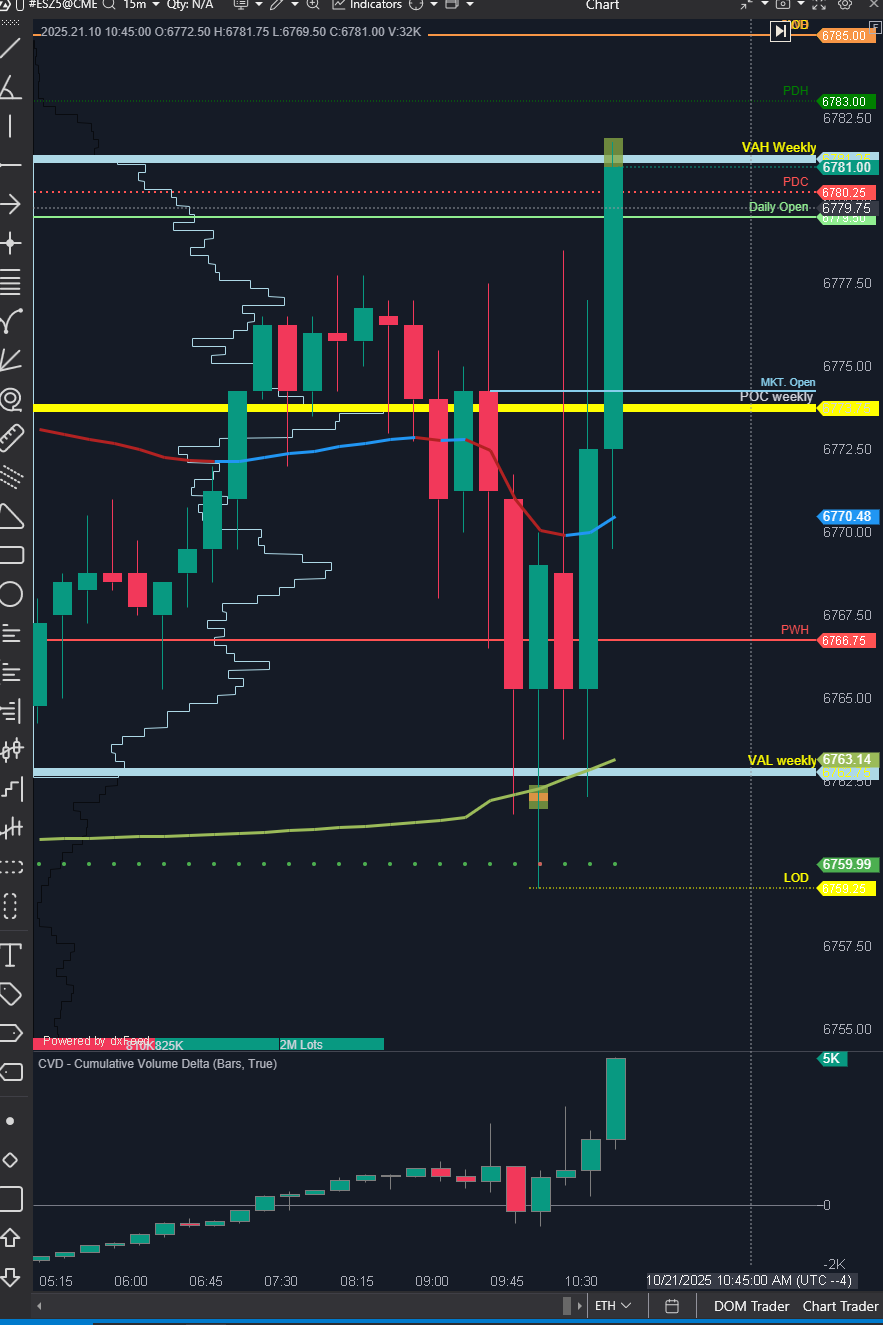

The market was trading in a tight range during pre-market hours following Monday's strong trending day that closed at session highs. This type of price action often sets up day 2 continuation patterns, creating an attractive environment for bullish positioning.

At market open, we saw classic institutional behavior with price immediately dropping to the low of day (LOD), effectively sweeping any resting liquidity that had built up overnight. I observed a large order getting filled at these lows, which is typically a sign of smart money accumulation at attractive levels.

Thesis & Plan

My thesis centered around a potential day 2 continuation play, leveraging the momentum from Monday's session. Given the tight overnight range and strong close the previous day, I expected any early weakness to be bought up aggressively.

The plan was to position for upside through long debit spreads on:

- MSTR - Strong momentum name with gamma characteristics

- SPY - Broad market exposure for the continuation theme

- IBIT - Under consideration as additional crypto/momentum exposure

Long debit spreads made sense in this environment as they offered defined risk while allowing participation in the expected gamma squeeze higher.

Entries & Exits

The key observation came at 10:21 AM when the market pushed above the opening price after completing the initial liquidity grab. This was the confirmation signal I was looking for that the day 2 continuation thesis was playing out.

The sequence was textbook:

- Market opens and immediately sells off to new LOD

- Large institutional order gets filled at the lows

- Price recovers and breaks back above opening level at 10:21 AM

This price action validated the setup and provided a clear entry signal for the debit spread positions.

Risk Management

Long debit spreads inherently provide defined risk, with maximum loss limited to the premium paid. This structure was appropriate given the setup, as it allowed for participation in the expected gamma move while capping downside exposure.

The timing of entries around the 10:21 AM breakout above opening prices provided a logical reference point for invalidation - if price failed to hold above the opening level, it would suggest the continuation thesis was not playing out as expected.

What Worked

The market read was accurate - we did see the classic day 2 continuation pattern unfold with the early liquidity grab followed by recovery. The institutional behavior at the lows (large order getting filled) was a strong confirmation signal that smart money was positioning for higher prices.

The debit spread structure was well-suited for this type of gamma squeeze environment, providing leveraged upside exposure while maintaining defined risk parameters.

What Didn't

The notes don't indicate any specific execution issues or failures in the setup. The pattern played out largely as anticipated with clear confirmation signals.

Lessons Learned

This trade reinforced several key principles:

Pattern Recognition: Day 2 continuation setups after strong trending days remain reliable, especially when combined with tight overnight ranges and opens at highs from the prior session.

Institutional Flow Reading: Watching for large orders getting filled during liquidity grabs provides valuable insight into where smart money is positioning. The large fill at the LOD was a clear signal that institutions were accumulating.

Timing Confirmation: Waiting for price to reclaim the opening level at 10:21 AM provided objective confirmation that the thesis was playing out, rather than trying to catch the exact bottom of the initial sell-off.

Structure Selection: Long debit spreads proved to be the right vehicle for this environment, balancing upside participation with risk management in a potentially volatile gamma squeeze scenario.

Multi-Name Approach: Considering correlated names like MSTR, SPY, and IBIT allowed for diversification of the same thesis across different instruments, potentially improving risk-adjusted returns.

The key takeaway is that patience in waiting for confirmation, combined with proper structure selection and institutional flow awareness, can create high-probability setups even in complex market environments.